The semiconductor industry is currently navigating a “once-in-four-decades shortage”, fuelling an unprecedented memory supercycle. While past memory booms were triggered by discrete technological leaps, such as the smartphone explosion in 2010, cloud buildouts in 2017 and the unexpected COVID-19 remote-work shock, today's cycle is more structural. It is being driven by non-linear demand for artificial intelligence (AI) infrastructure, reshaping both the pricing and strategic landscape of the global memory market (Semi Analysis, 02/2026).

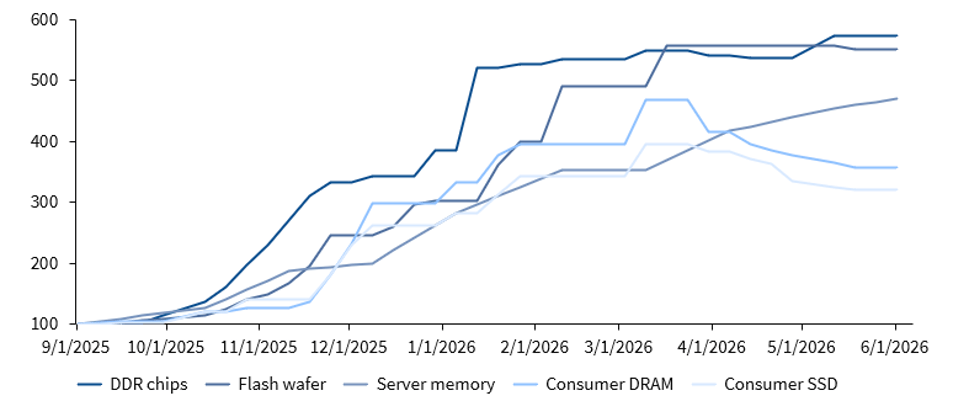

KnowledgeAgent analysis of ChinaFlashMarket spot-price data shows a broad memory price reset since September 2025. The strongest increases occurred upstream: DDR chips rose by 473% and flash wafers by 452% over nine months. Downstream categories also increased sharply, from 221% for consumer SSDs to 369% for server modules, although pass-through has been more differentiated due to inventories, contract timing, Bill of Materials (BOM) mix and channel competition.

Figure 1: Indexed price development of select memory products, 100% = 9/1/2025

This evidence supports the central argument of the current supercycle: AI demand is tightening supply at the fab and wafer level, causing the impact to cascade into DRAM, NAND, server memory, SSDs and consumer devices.

Reasons for the supercycle

This supercycle is underpinned by a massive supply-demand mismatch, heavily influenced by physical scaling limits and changing compute architectures.

On the demand side, the industry is transitioning from simple generative LLM outputs to Agentic AI workloads. Agentic AI involves complex orchestration, tool planning, and continuous sequential execution, which shifts the computing bottleneck more directly from the GPU to the CPU and memory hierarchy. This requires massive High Bandwidth Memory (HBM) for processing and immense enterprise storage, as maintaining conversational context for AI agents consumes vast memory resources (Morgan Stanley, 03/2026; BNP Paribas, 03/2026).

On the supply side, the supercycle is sustained by intense capital discipline. Memory fabs require multi-billion-dollar investments and multi-year construction timelines. Today, capacity is not being added fast enough due to floor space constraints, lengthening equipment lead times and the sheer difficulty of scaling advanced node physics. Top manufacturers are systematically prioritizing highly lucrative AI components, leaving legacy and consumer segments starved for wafer allocations (BNP Paribas, 03/2026; UBS, 03/2026; Semi Analysis, 02/2026).

The result is a market in which upstream pricing moves first. Raw wafers and chips have repriced earlier and more sharply than finished products, while downstream pass-through is delayed by existing inventories, contracts, and channel competition. This explains why recent data already shows extreme increases in DDR chips and flash wafers, while consumer SSDs and consumer DRAM show a more lagged and uneven response.

Estimates on cycle duration

Because supply cannot easily adjust to meet structural AI demand, experts estimate this supercycle will be exceptionally durable.

DRAM undersupply is expected to persist at least until the fourth quarter of 2027, with some industry participants anticipating constraints extending into 2028 and beyond. NAND is following a similar pattern, with the expected cycle peak pushed outward and supply-demand balance or surplus not expected until mid-to-late 2027 or 2028 (Morgan Stanley, 02/2026; UBS, 03/2026).

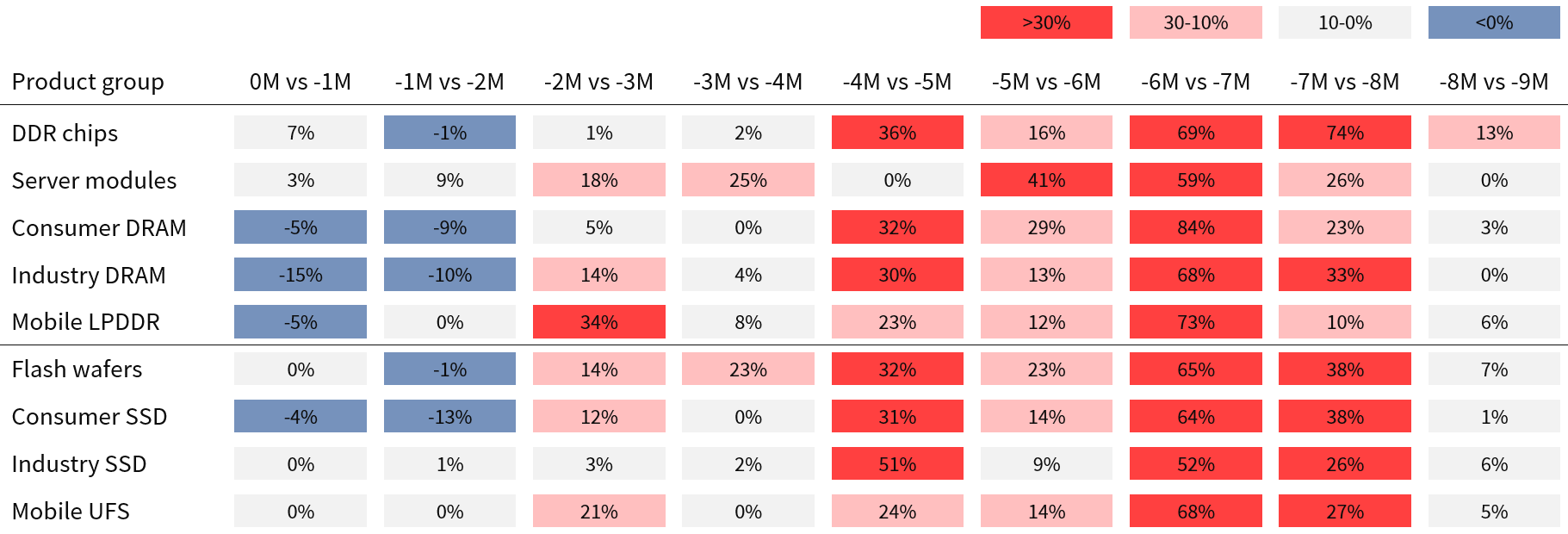

The latest price data suggests that the market has already passed through the steepest phase of the initial reset, but not necessarily that the cycle is normalizing. Monthly data shows that the strongest price shock occurred between October 2025 and January 2026.

Since spring 2026, momentum has cooled down. The latest month shows flat to modest changes in most NAND categories and small declines in selected consumer and industrial DRAM products. However, this moderation follows a much larger earlier reset. Absolute price levels remain highly elevated versus September 2025, and another downstream pass-through wave remains possible if upstream DDR chip and flash wafer prices do not stabilize.

Figure 2: Monthly price movement by product category, %, 0M = June 2026

Effects across segments: DRAM vs. NAND

The effects of this supercycle vary across memory types:

- DRAM: AI accelerators and custom cloud ASICs, such as AWS Trainium and Google TPU, consume vast quantities of memory. HBM bit demand is forecast to grow by 66% in 2026 and 62% in 2027 (BNP Paribas, 03/2026). This demand shock is reflected in broader DRAM pricing. KnowledgeAgent analysis shows that DDR chips increased by 473% over nine months, while server modules rose by 369%, consumer DRAM by 257%, mobile LPDDR by 286% and industrial DRAM by 196%.

- NAND: Enterprise SSD (eSSD) has emerged as the primary growth driver for NAND, essentially acting as memory to offload data from expensive HBM setups. Solutions such as NVIDIA's Inference Context Memory Storage (ICMS) use specialized data processing units to manage up to two petabytes of NAND per rack for agentic AI context retention. As a result, eSSD contract pricing is expected to roughly double in the first half of 2026 alone (BNP Paribas, 03/2026; Morgan Stanley, 03/2026). The spot-price data confirms that NAND is also exposed to the broader memory reset. Flash wafers rose by 452% over nine months, while consumer SSDs increased by 221%, industrial SSDs by 253% and mobile UFS by 283%. This shows that the price shock is not limited to AI-relevant products.

There are early signs of category-specific correction pressure. Over the last three months, consumer DRAM fell by 10% and consumer SSDs by 7%, while some industrial DRAM categories also declined. However, these corrections should be read as stabilization after a large price reset rather than a return to normal. Upstream prices remain far above September 2025 levels, and the pass-through into finished products may continue as contracts, inventories and channel prices adjust.

The surging cost of server memory upgrades

To keep up with the immense data demands of AI, data centers are shifting toward advanced memory technologies, including high-performance DDR5 and new modular designs like SOCAMM (Small Outline Compression Attached Memory Module).

While these new modules deliver significant bandwidth and power efficiency improvements over traditional server hardware, they come at a steep financial premium during the current supply shortage (BNP Paribas, 03/2026).

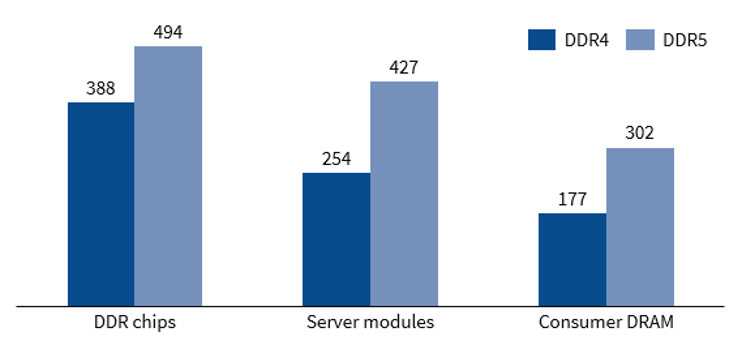

The cost growth in server memory has been explosive, driven by strong cloud provider demand. KnowledgeAgent analysis shows that server modules increased by 369% over nine months, making server memory one of the strongest downstream price movers in the dataset. This upward pressure is especially visible in DDR5. Across all shown DRAM categories, DDR5 repriced more strongly than DDR4: DDR5 DDR chips increased by 494%, DDR5 server modules by 427% and DDR5 consumer DRAM by 302%. By comparison, DDR4 increased by 388%, 254% and 177% in the same categories.

Figure 3: 9-month price increase of DRAM memory generations, %

The widening DDR5 premium is consistent with the current AI infrastructure cycle. AI servers and newer data-center platforms require higher-performance memory architectures, making demand for DDR5 more pronounced than for older DDR4 products. DDR4 prices remain highly elevated, but the driver is different. DDR4 benefits from general market tightness and spillover from constrained supply, while DDR5 is more directly exposed to incremental AI server demand, platform transitions, and tighter availability of newer-generation components.

Furthermore, highly advanced new formats like SOCAMM are commanding premium valuations, pricing at roughly 25% to 33% of the cost of the expensive High Bandwidth Memory (HBM) chips used directly in AI GPUs. This massive inflation in enterprise server memory costs underscores the intense competition among buyers to secure advanced infrastructure, regardless of the price tag (BNP Paribas, 03/2026).

The squeeze on home PCs and mobile phones

While AI infrastructure is pulling advanced memory capacity toward data centers, consumer electronics are bearing much of the cost pressure. The steep rise in memory costs is putting significant pressure on hardware margins for consumer device OEMs (Morgan Stanley, 02/2026).

Prior to mid-2025, memory represented just 10% to 15% of the BOM cost for smartphones and PCs. By the first quarter of 2026, memory is projected to account for 25% to 35% of smartphone BOM costs and 20% to 22% of PC BOM costs (BNP Paribas, 03/2026).

KnowledgeAgent’s price data shows why this pressure is now becoming visible beyond data centers. Consumer DRAM rose by 257% over nine months, consumer SSDs by 221% and mobile UFS by 283%. Even though consumer DRAM and consumer SSDs have shown some recent correction, their price levels remain far above September 2025. For OEMs, this creates a difficult trade-off: raise retail prices on high-end models, downgrade memory specifications on low- and mid-tier devices or accept lower margins (BNP Paribas, 03/2026).

Consequently, this cost inflation risks real demand destruction. Analysts forecast global smartphone and PC shipments could decline by 1% to 5% in 2026 as consumers delay hardware upgrades due to higher upfront costs and limited specification improvements (BNP Paribas, 03/2026; Morgan Stanley, 02/2026).

Conclusion

The current memory boom represents a paradigm shift. Rather than chasing pure volume, suppliers are exercising extreme capacity discipline to feed high-margin AI segments. This is creating a broader repricing across the memory value chain, with upstream chips and wafers absorbing the sharpest reset before downstream products follow.

The key lesson from the data is that this is not only an HBM story. DDR chips, flash wafers, server modules, consumer DRAM, consumer SSDs, industrial products and mobile memory formats have all been affected. AI demand is tightening the market at the capacity level, and the resulting cost pressure is cascading into products that are only indirectly linked to AI.

While this supercycle enriches memory fab owners with historically high operating margins, it simultaneously acts as a steep inflationary tax on consumer electronics. Memory has become a strategic bottleneck for the AI era, and its cost is starting to show up across the digital economy.

For companies exposed to electronics, semiconductors, cloud infrastructure, industrial equipment or consumer devices, the memory supercycle has implications for sourcing, pricing, product configuration, margin management, and competitive positioning.

At KnowledgeAgent, we track how shifts in technology markets translate into commercial risks and opportunities. If your business is exposed to memory pricing, AI infrastructure demand, or semiconductor supply constraints, we can help assess what this means for your market and strategic decisions.

- BNP Paribas, 03/2026, NANDriving the memory super-cycle

- Morgan Stanley, 02/2026, AI boosts NAND demand, but Asian module maker margins may soon compress

- Morgan Stanley, 03/2026, Memory – Exponential Agentic

- Semi Analysis, 02/2026, Memory Mania: How a Once-in-Four-Decades Shortage Is Fueling a Memory Boom, https://newsletter.semianalysis.com/p/memory-mania-how-a-once-in-four-decades, accessed 06/11/2026

- UBS, 03/2026, Memory Semis Monthly: March ‘26 Edition: Strong memory pricing momentum continues unabated